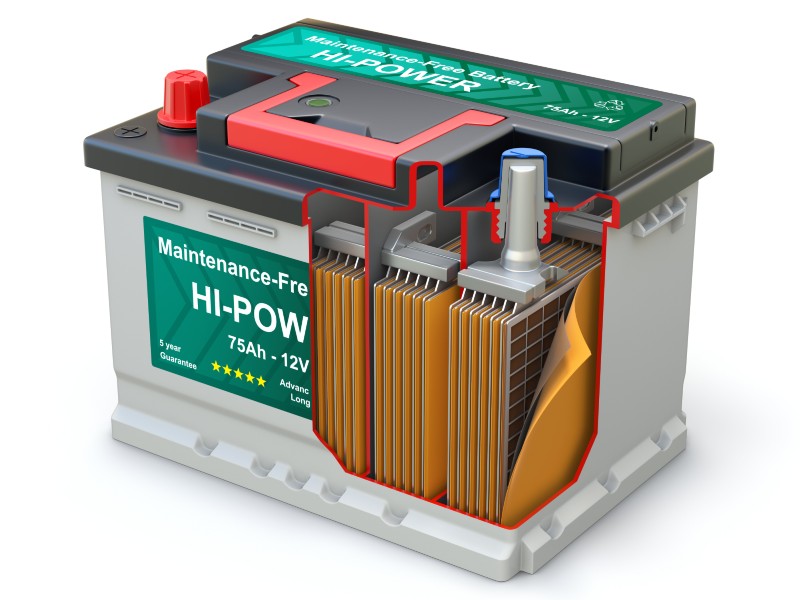

Due to its toxic legacy, lead is probably the last metal that one associates with green technology. However, lead-acid batteries are still a key component in the automotive industry as well as for energy storage.

According to an article on Euractiv.com, even more pure electric vehicles use lead-acid batteries for starting, lighting and ignition (SLI) as well as for other functions such as electronic door-locking and in-car entertainment. Furthermore, its proven reliability makes it the metal of choice for energy back-up services in hospitals, emergency services and public buildings.

The article further states that constraints on lithium-ion battery production to meet EV demand over the coming years opens the energy storage market to “other battery technologies” such as those using lead. So, what does this mean for lead going forward?

Increase in production predicted

A Wood Mackenzie report states that the naturally resilient nature of lead demand, honed by decades of substitution pressure, enabled lead to mitigate the worst impacts of the pandemic and rebound strongly as the world recovered.

After a poor 2019, with its 0.5% demand drop, coronavirus-hit 2020 consumption dipped prices only 3.2%.

Demand recovered well and is forecast to enjoy a 4.2% rebound during 2021, followed by an average of 2.3% per annum for the three years after that.

One of the key reasons for this is that half of all lead consumption goes for automotive replacement batteries. These aren’t discretionary purchases: when a vehicle battery fails, it must be replaced for that vehicle to remain usable. In the first weeks of global lockdowns, replacement demand dipped sharply as populations stayed home, as did their cars.

But then, as people ventured out again, many found that weeks or months of not using their car had caused the battery to fail. The consequent surge in automotive battery demand has endured since, particularly in North America and Europe, and has more than offset the fall in OEM battery requirement caused by microchip shortages and other pandemic-related factors.

Meanwhile, lead production suffered pandemic effects on raw materials supply from mines for primary smelters and scrap feed to secondary plants. Mine curtailments or closures impacted global mine output, which plunged 7.9% year-on-year in 2020, but a 5.4% recovery is predicted this year.

However, this will still be the lowest volume of concentrate production since 2012. Primary smelter output actually increased in 2020 over the previous year, due to a large overhang of concentrate stocks from the end of 2019. This provided good volumes of feed to compensate for sagging mine production.

According to the report, global concentrate stocks are currently somewhat tight and this situation will not improve over the next couple of years as mine output struggles to build momentum. It will take until the middle of this decade before primary smelters are well-supplied.

The primary concern about lead is that it is highly toxic and cases of lead poisoning have been well documented over the decades. Still, it has a key role to play both in the EV space and other sectors that rely on battery storage for the foreseeable future.